Introduction

This survey, conducted with the participation of 1,045 women from 29 provinces of Afghanistan, provides a comprehensive and detailed picture of women’s purchasing power, savings capacity, sources of income, and their economic limitations. The findings indicate that women’s purchasing power—especially among unemployed women—has declined over the past three years, and the economic crisis has had profound impacts on households.

Key findings

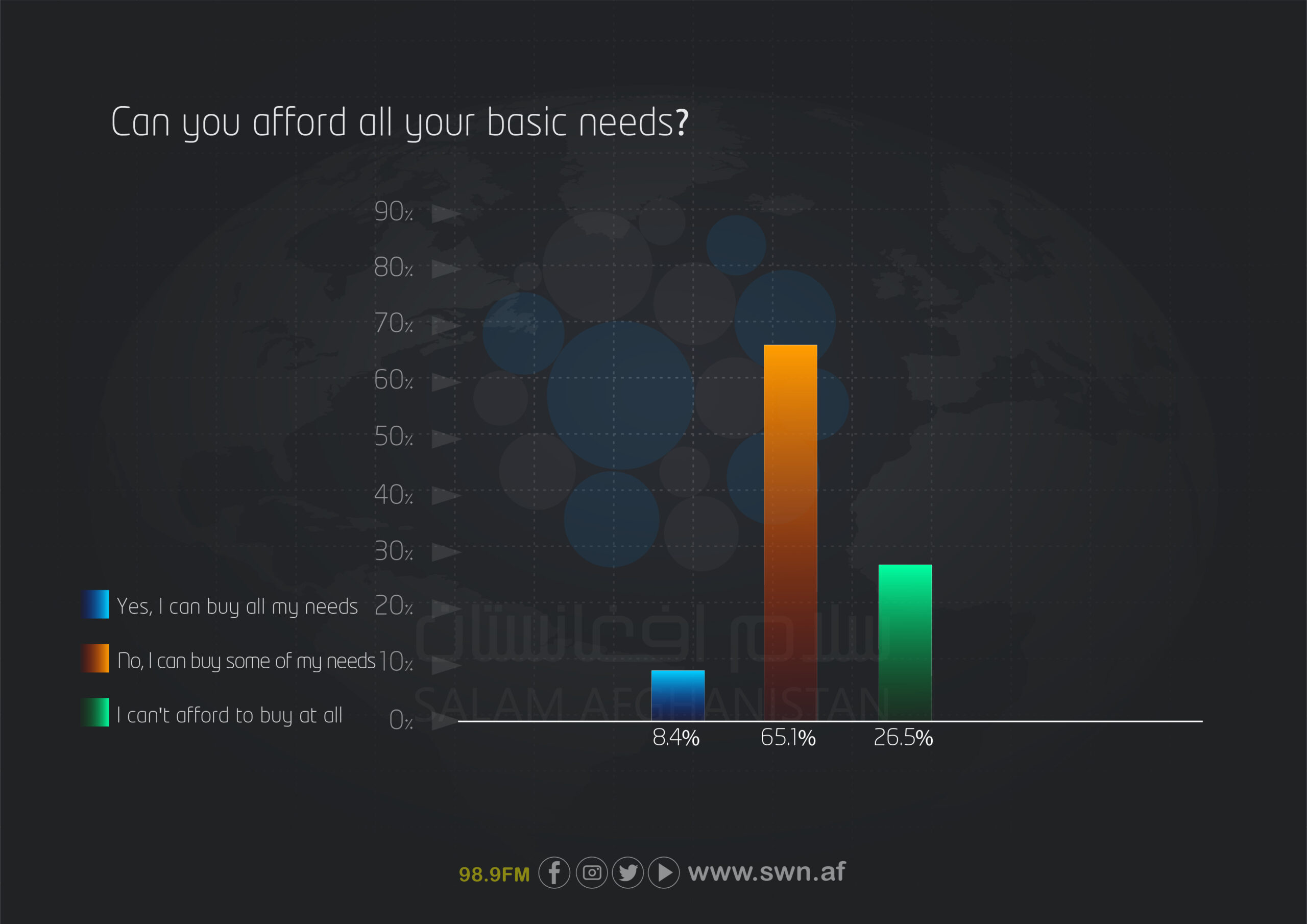

- Nearly 26.5% of respondents have no purchasing power at all, while 65.1% can meet only some of their needs. Only 8.4% are able to purchase all of their necessities.

- Among unemployed women, 32.8% have no purchasing power, compared to 14.8% among employed women.

- More than 72% of unemployed women and 61% of employed women are unable to save money.

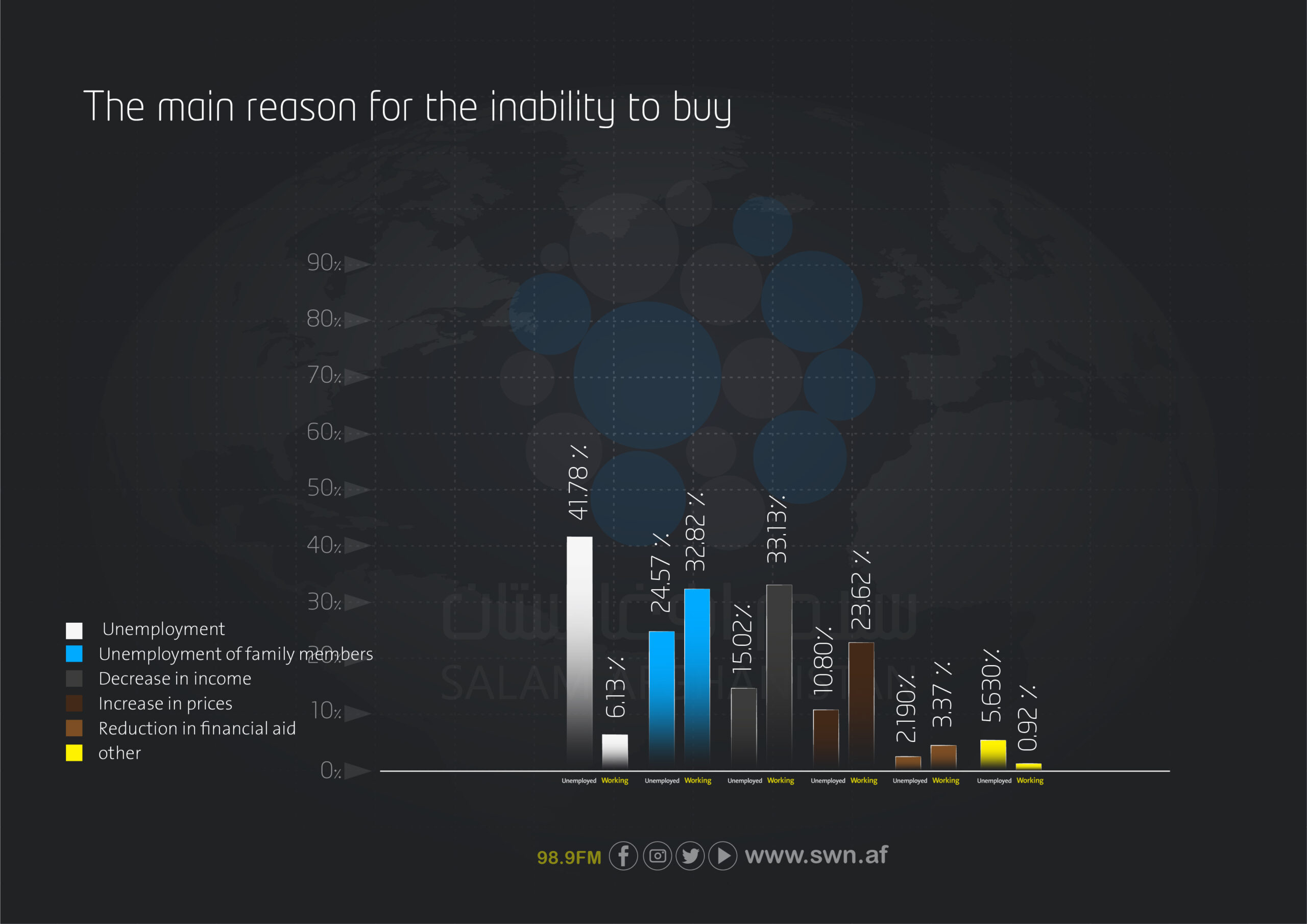

- The main reasons for inability to purchase are: personal unemployment (about 41% among the unemployed), and for employed women, particularly reduced income and rising prices (about 33% and 24%, respectively).

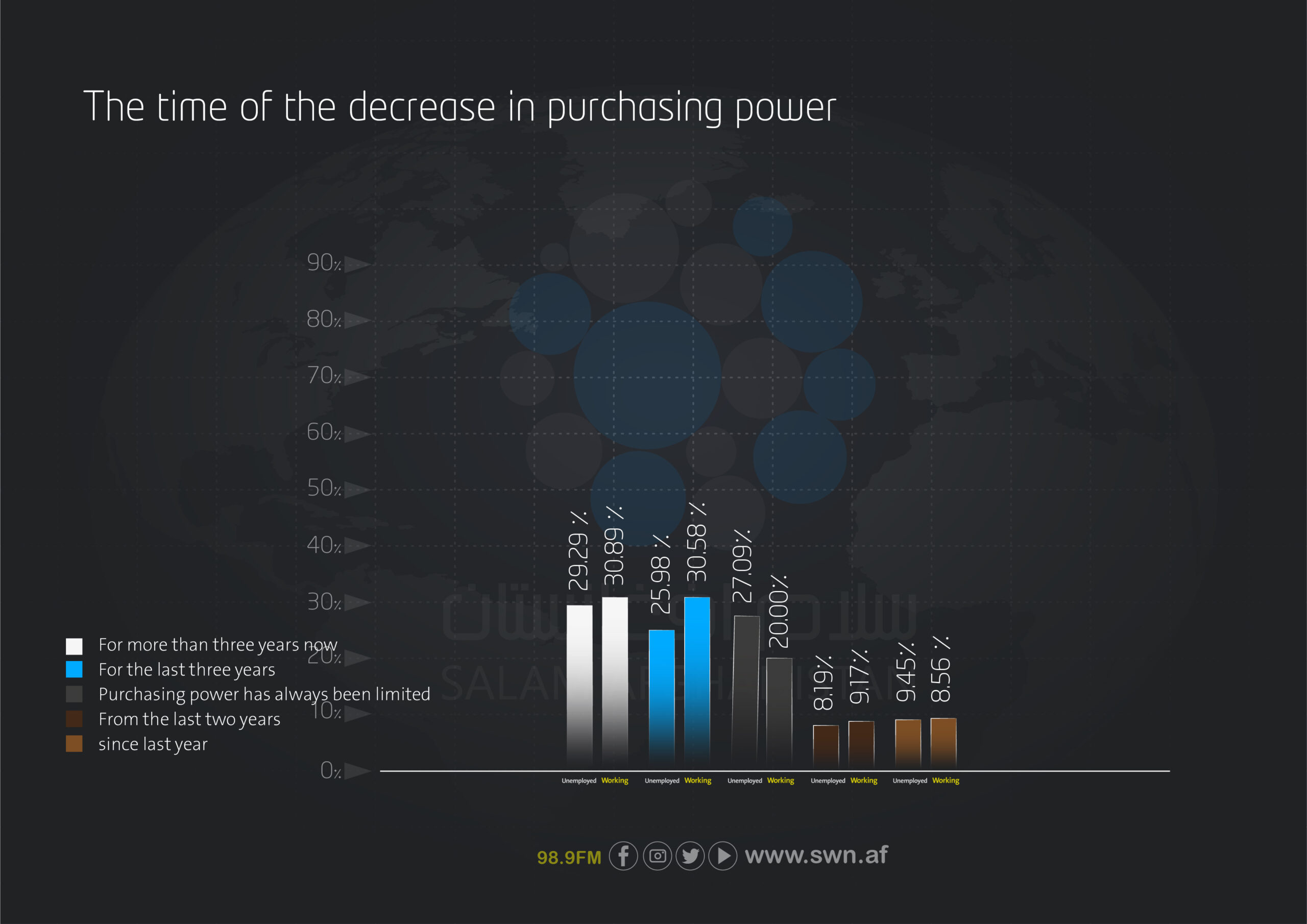

- For more than 55% of respondents, economic constraints date back more than three years or have always been present.

Survey objectives

General objective: To conduct a comprehensive assessment of women’s purchasing power.

Specific objectives:

- To evaluate the status of women’s purchasing power in Afghanistan.

- To examine the extent to which essential household expenses are covered.

- To compare the economic conditions of employed and unemployed women.

- To identify sources of income and how they are utilized.

- To determine the main causes of financial and purchasing constraints.

- To provide data-driven recommendations for policymakers and support organizations.

Research methodology

- Statistical population: Women divided into two groups—employed (364 participants) and unemployed (681 participants)—with a total of 1,045 respondents.

- Sampling method: Multi-stage cluster–stratified sampling.

- Data collection tool: A structured questionnaire consisting of demographic characteristics, employment status, income, adequacy of expenses, savings, and purchasing power.

Sample size: The study sample consisted of 1,045 employed and unemployed women.

Data collection tool

The data collection tool for this survey was a structured questionnaire, designed to gather precise information regarding women’s purchasing power. The questionnaire included the following sections:

- Demographic characteristics (6 questions)

- Sources of income and household expenses (5 questions)

- Income level and adequacy (1 question)

- Consumption patterns and main expenditures (2 questions)

- Purchasing power and reasons for limitations (2 questions)

Research period: The survey was conducted over five months, from March to August 2025, in the provinces of Afghanistan.

Publication date: July–August 2025

Definition of purchasing power

In this survey, inability to purchase refers to households that, due to unemployment, reduced income, or rising prices, are unable to fully meet basic needs such as food, clothing, healthcare, and house supplies.

Study limitations

- Limited access to some remote areas due to complex geographical conditions and time constraints.

- Lack of comprehensive historical data on women’s purchasing power for more precise analyses.

- Financial and human resource limitations, preventing coverage of all districts.

- Lack of accurate and systematic economic and price-based data for all the study areas.

Comprehensive abstract of the survey on women’s purchasing power

This survey was conducted to examine women’s purchasing power across different regions from March to August 2025. Data were collected through a structured questionnaire that included questions on demographic characteristics, economic impacts, and factors influencing women’s purchasing power. The survey findings indicate that multiple factors, including household income and access to financial and social support, play a significant role in determining women’s ability to purchase necessities. According to the results, women’s purchasing power has sharply declined in recent years.

Key findings

Only 8.4% of respondents are able to purchase all their basic needs, while 91% are unable to purchase. Among these, 65.1% can meet only some of their needs, and 26.5% cannot meet any basic needs. These data highlight significant financial limitations for most families.

Findings show that more than two-thirds of the women surveyed reported a decline in their purchasing power compared to previous years. One of the most important factors affecting purchasing power is household income, and it is influenced by various economic and social factors.

Nearly 72% of participants reported a decline in their purchasing ability in recent months, primarily due to reduced household income. Employment status also positively impacts women’s ability to purchase necessities.

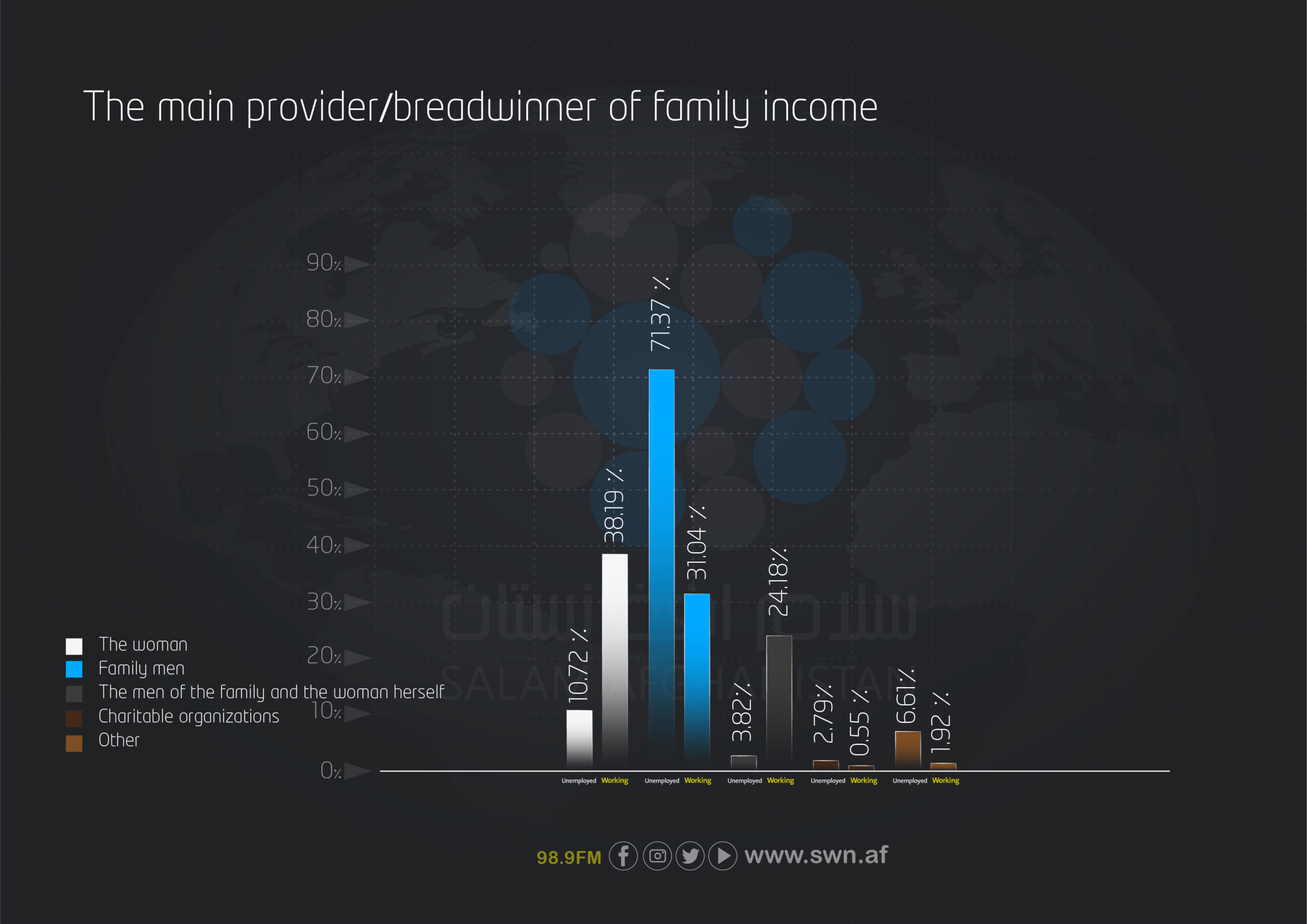

Among unemployed women, 71.37% told that men in the family are the primary income providers, while only 10.72% consider themselves responsible for income. Among employed women, 38.19% are the main earners, and 24.18% share this role with male family members.

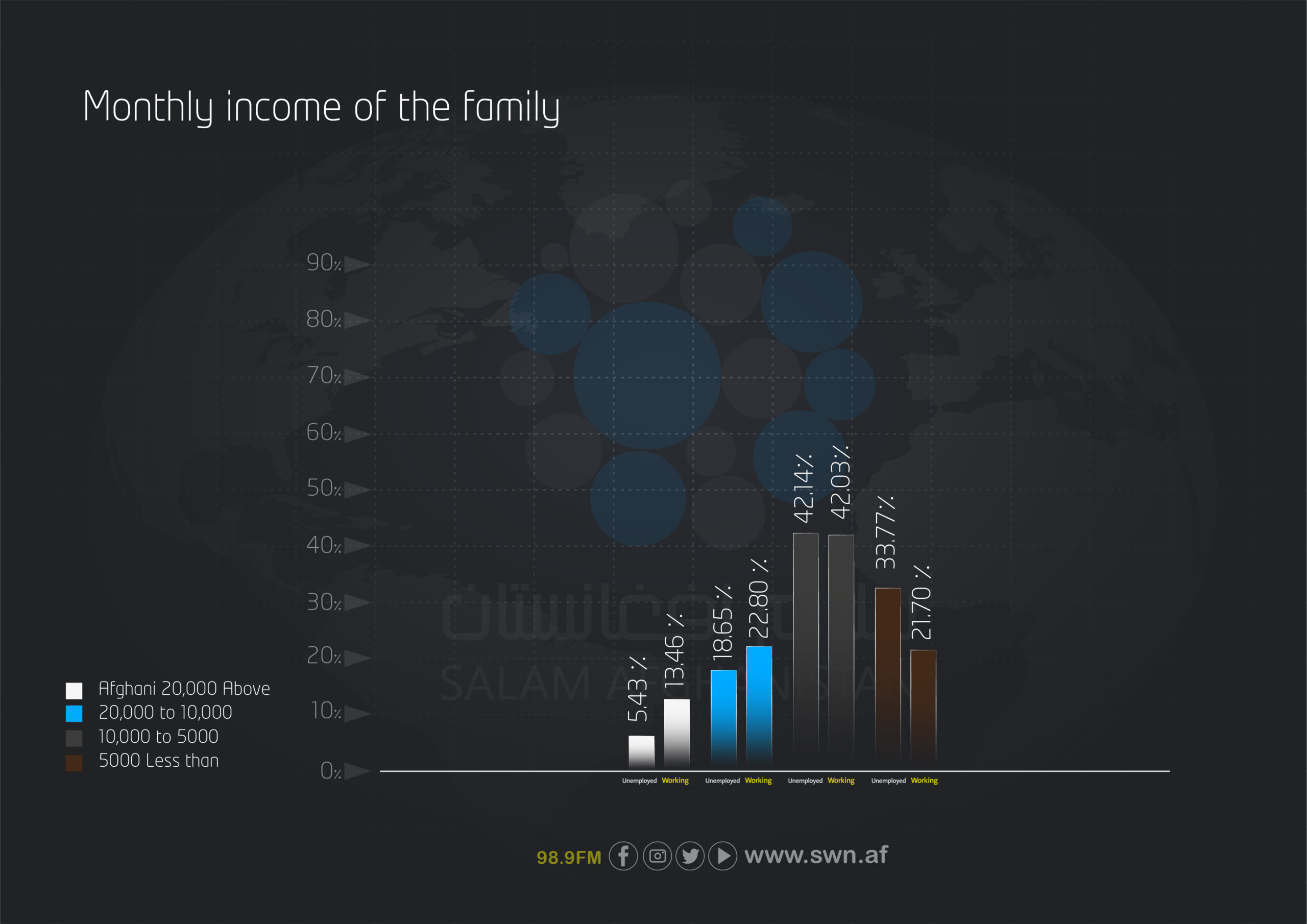

Most families in both groups earn less than 10,000 Afghanis (unemployed: 75.91%, employed: 63.73%). Only 5.43% of unemployed and 13.46% of employed women report incomes above 20,000 Afghanis.

Lack of savings capacity is a major challenge, with 78.56% of unemployed and 62.71% of employed women reporting that they are unable to save at all.

Food, clothing, and healthcare consume the largest share of household income. In both groups, more than half of respondents told that food is the first most expensive necessity, especially when combined with costs for healthcare, education, and household items.

The survey underscores the urgent need to improve women’s livelihoods through economic empowerment programs, targeted livelihoods support, creation of sustainable employment opportunities, and development of support networks. Without effective interventions, the economic gap and financial dependency of women in society will continue to widen, leading to broader social and economic consequences.

Overview of women’s purchasing power in Afghanistan

Report summary

The findings of this survey, conducted with the participation of 1,045 women from 29 provinces of Afghanistan, depict a worrisome picture of Afghan women’s purchasing power under current economic conditions.

More than 66% of Afghan women are unemployed, with only one-third engaged in work. This employment gap has reduced their purchasing power and increased financial dependency. Among unemployed women, over 71% of household income is provided by men, whereas among employed women, about 38% are the primary earners in their families.

Declining household income is also a widespread concern. Women surveyed reported that their monthly income is less than 10,000 Afghanis, which is barely sufficient to meet basic needs. As a result, over 68% of unemployed women and 60% of employed women stated that they have no capacity to save.

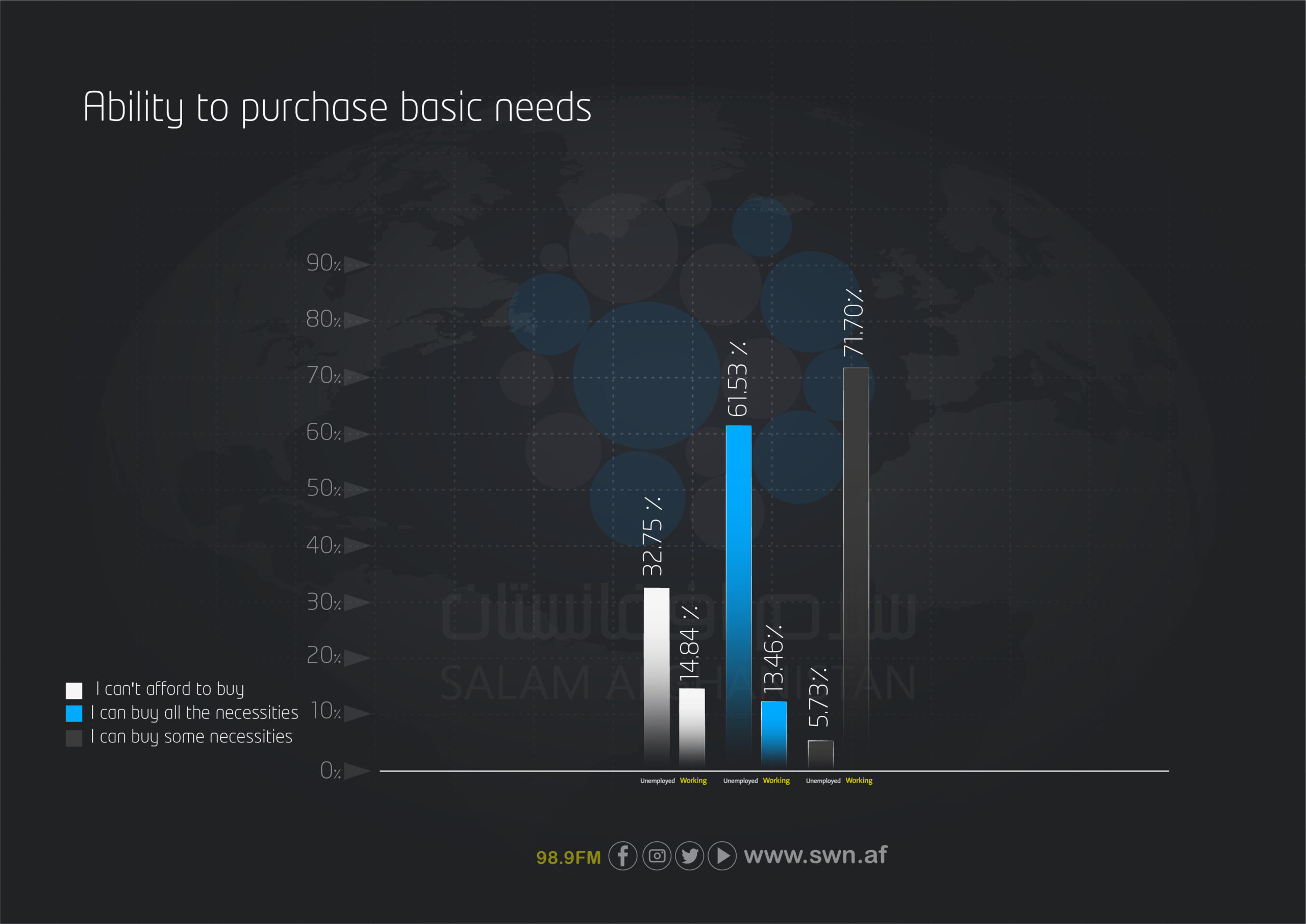

The ability to purchase basic necessities such as food, clothing, healthcare, and household items is severely limited. Among unemployed women, more than 32% reported having no purchasing power at all, and only 5.7% can afford some of their needs. Among employed women, over 70% stated that they are only able to buy part of their required items.

Regarding the types of items women cannot purchase, among employed women, 21.3% are unable to buy household items, and more than 9% cannot cover healthcare expenses. Among unemployed women, the greatest inability is seen in purchasing food, clothing, and healthcare, with the combined total exceeding 45%.

The main reasons for reduced purchasing power include personal unemployment, unemployment of family members, and decreased household income.

Overall report

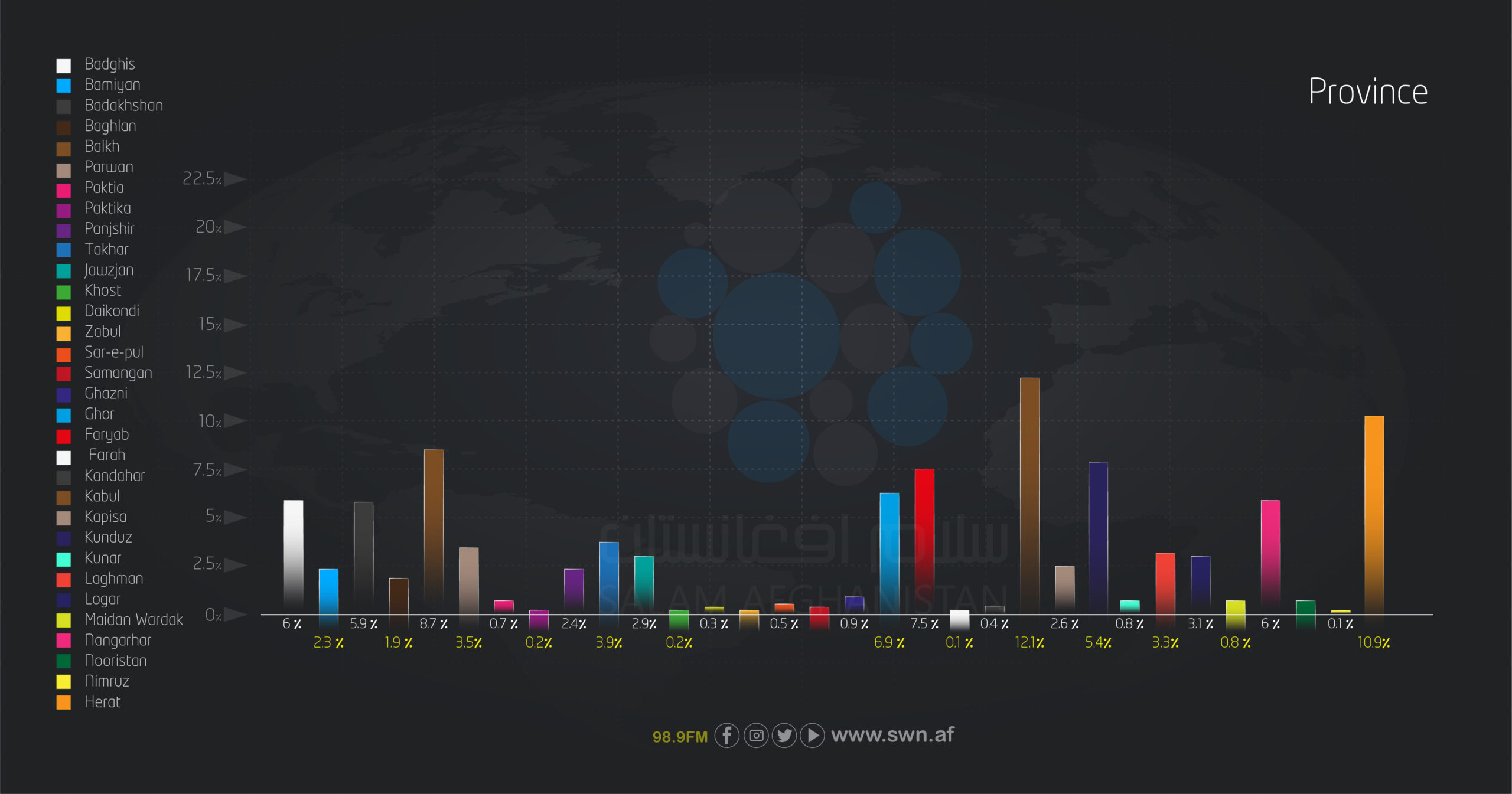

In this survey, 1,045 women from 29 provinces of Afghanistan participated. Kabul accounted for the largest share with 12.1% (126 participants), followed by Herat with 10.9% (114 participants) and Balkh with 8.7% (91 participants). Farah and Nimroz provinces had the smallest participation, each contributing less than 3% of the respondents.

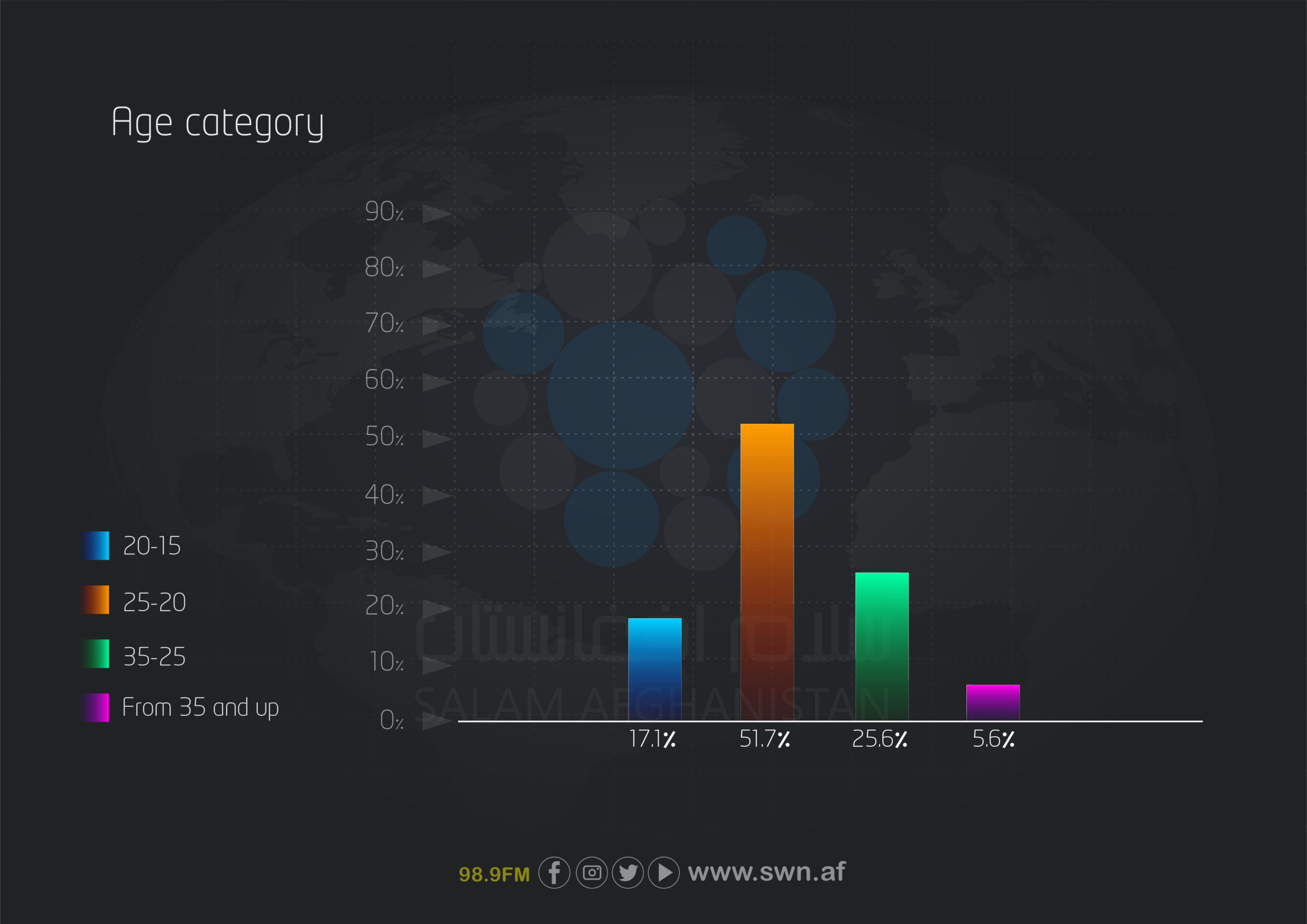

The largest group of women participating in this survey falls within the 20 to 25-year-old age range, with 540 participants (51.7%). This is followed by the 25 to 35 age group with 268 participants (25.6%) and the 15 to 20 age group with 179 participants (17.1%). Only 5.6% (58 participants) are over 35 years old. These data indicate that young women are the most represented in this sample.

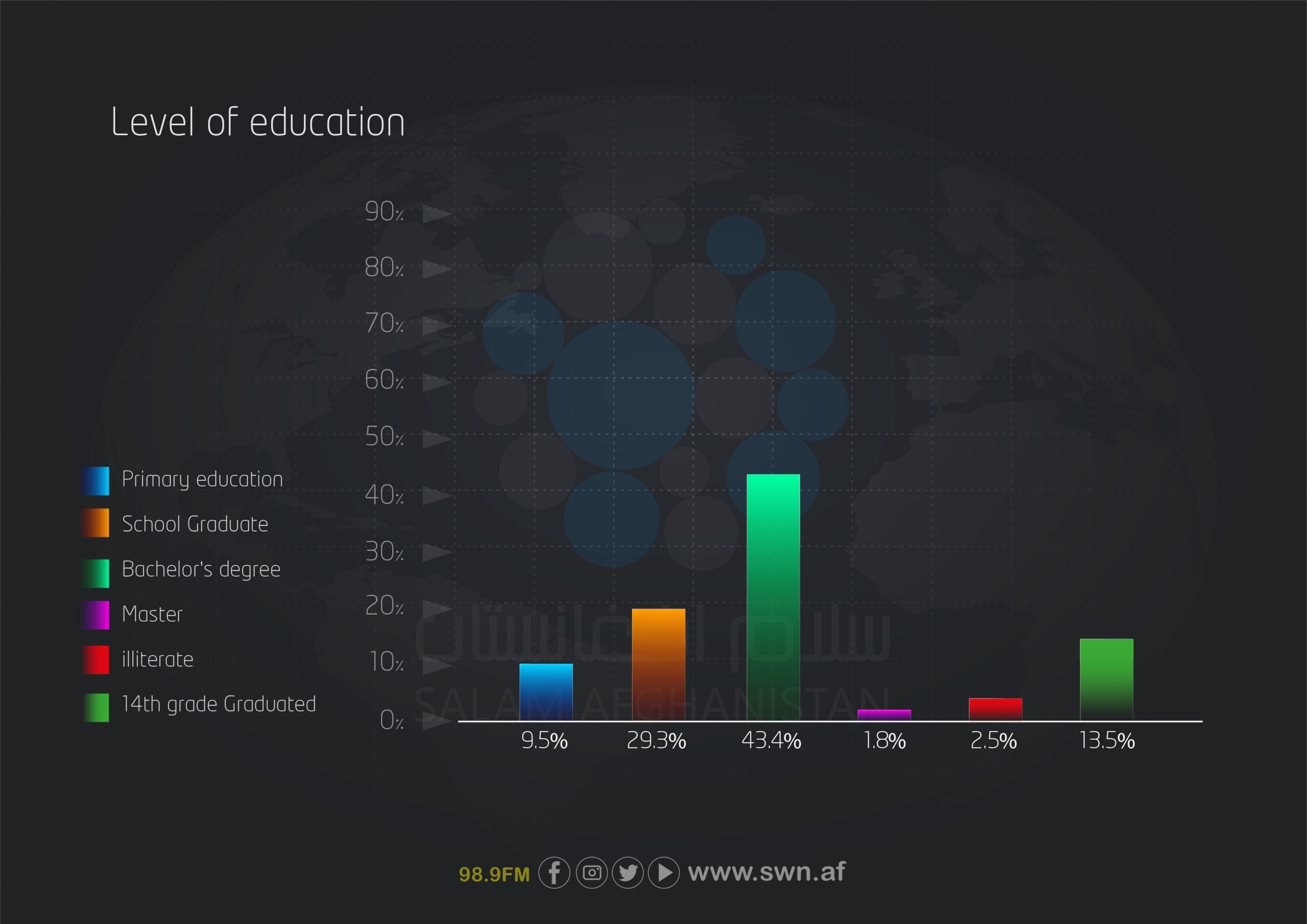

A significant number of women participating in this survey have secondary and higher education. The largest group of respondents, 454 women (43.4%), hold a bachelor’s degree, followed by 306 women (29.3%) who have completed 12th grade, and 141 women (13.5%) who have completed 14th grade. On the other hand, 99 women (9.5%) have only primary education, 26 women are illiterate, and 19 women hold a master’s degree.

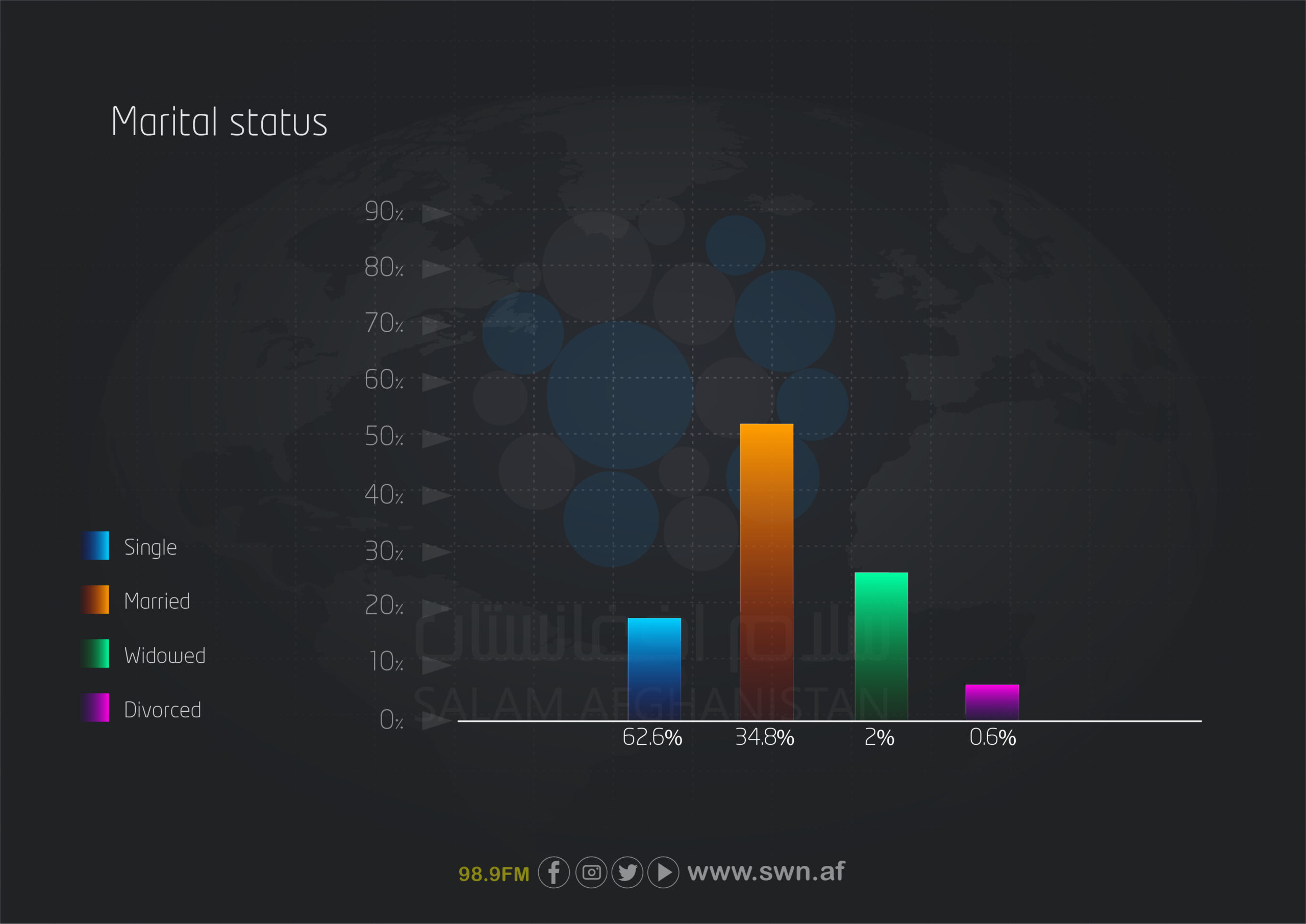

In this survey, the majority of respondents were single, comprising 62.6% of participants, while 34.8% were married, 2% were widowed, and 0.6% were divorced. These statistics indicate that single women represent a large portion of the target population, and marital status may influence women’s consumption patterns and economic decision-making.

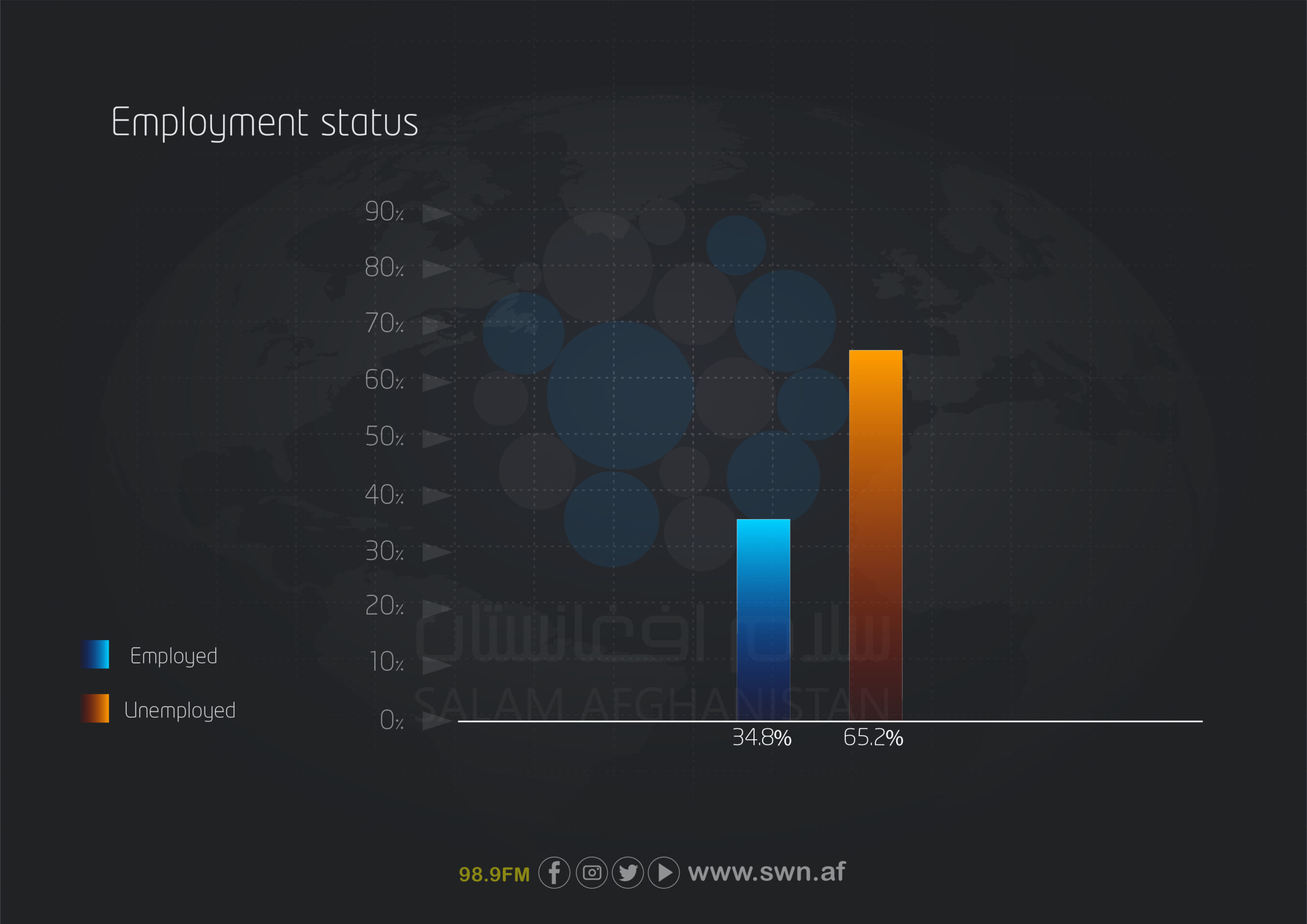

In this survey, 65.2% of women are unemployed while 34.8% are employed. This finding indicates that a large portion of the participating women are not active in the labor market. Employment status can have a significant impact on women’s purchasing power and overall economic situation.

The largest share of respondents, 54.7%, come from families with 5 to 10 members. Smaller families with 1 to 5 members account for 28.8%, larger families with 10 to 15 members make up 13.3%, and only 3.2% of respondents come from families with more than 15 members. These data reflect the diversity of family sizes within the target population.

Only 8.4% of respondents are able to purchase all of their basic needs, while the remaining 91% are unable to purchase. Among these, 65.1% can meet only some of their needs, and 26.5% cannot meet any basic needs at all. These data indicate a significant financial limitation for the majority of families.

More than half of the respondents (57.1%) cited their own or family members’ unemployment as the main reason for their inability to purchase necessities. This was followed by reduced income (21.1%) and rising prices (15.1%). These findings indicate that employment and income are key factors in determining a household’s purchasing power.

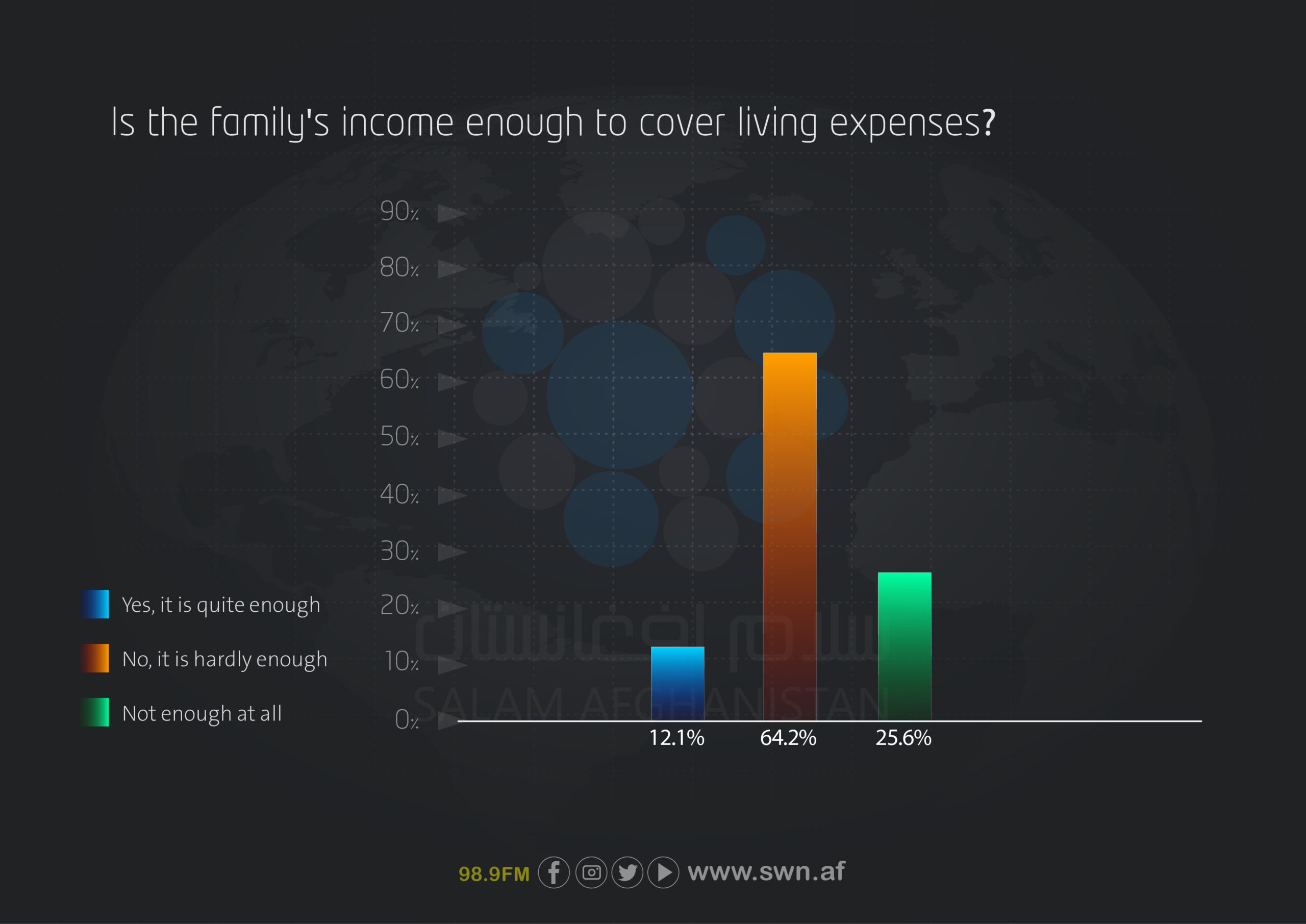

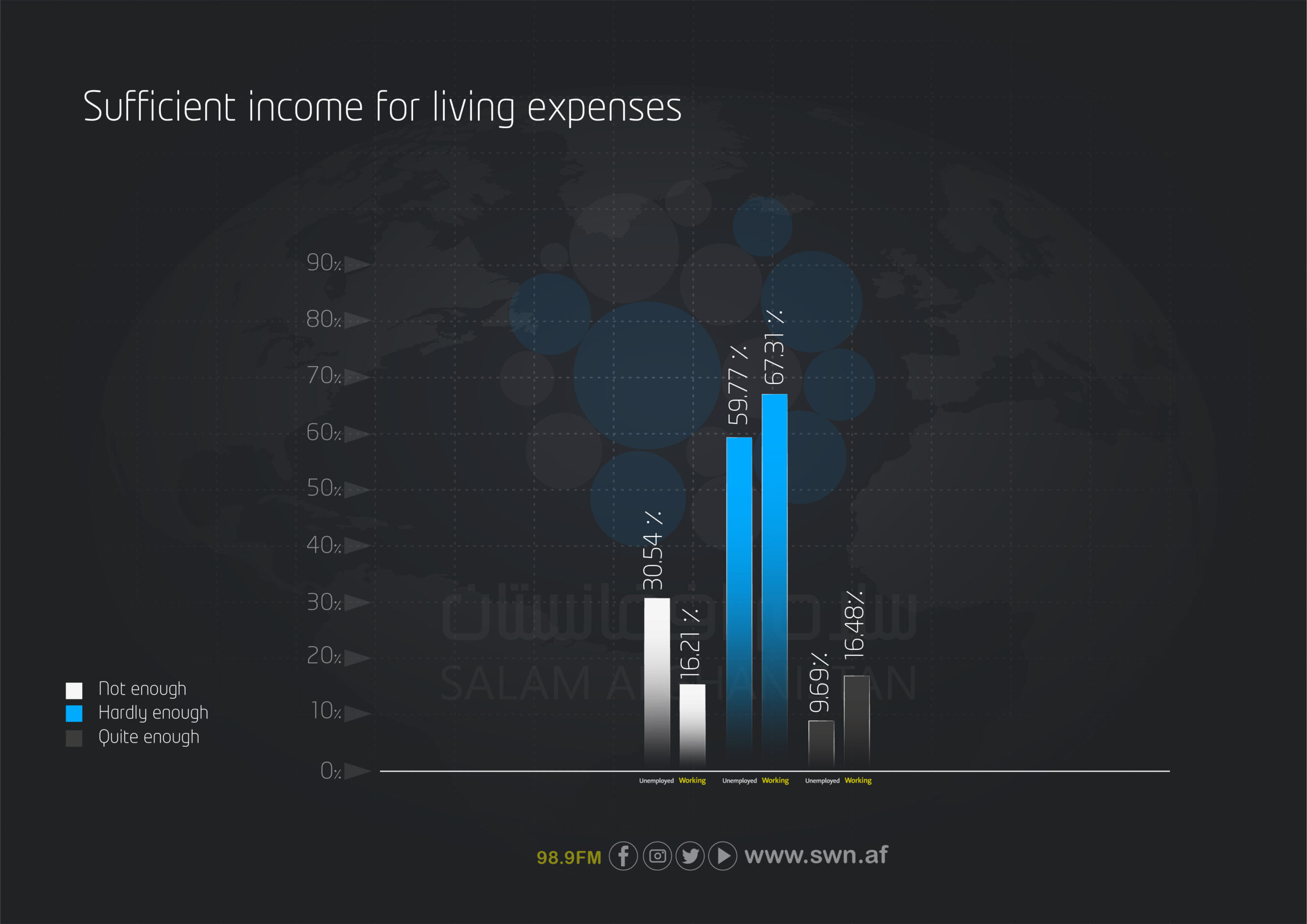

Among the women participating in the survey, 89.8% reported that their household income is insufficient to cover living expenses. Of these, 64.2% stated that it “barely meets needs” and 25.6% said it is “completely insufficient,” while only 12.1% indicated that their income is fully sufficient. This reflects the severe economic pressure on households.

According to the survey results, the greatest challenges in purchasing are related to household items, with 35.4% of respondents reporting that they are unable to afford them. Nearly 19% of women face difficulties in covering healthcare needs, and about 14% struggle to purchase food. These findings highlight the severe economic pressure and financial constraints in meeting families’ basic needs, which directly affect their quality of life.

The largest portion of household income is allocated to food, cited as the main expense in more than 36% of responses. This is followed by children’s education, accounting for approximately 27%, and healthcare, with nearly 19%. These results indicate that the majority of family income is spent on essential and vital needs, leaving very little room for other expenses.

Nearly 72% of families have a monthly income of less than 10,000 Afghanis; about 20% of families earn between 10,000 and 20,000 Afghanis, and only 8.2% report an income above 20,000 Afghanis. These figures reflect the widespread economic limitations and low incomes among the majority of families participating in the survey.

Men in the family play the primary role in providing household income, with about 57.3% of respondents indicating this. Approximately 20.3% of women reported being solely responsible for their family’s income. Additionally, combined arrangements such as “family men and myself” account for 10.9%, while the role of institutions or charitable individuals contributes less than 5%. These figures show that household income largely depends on male family members.

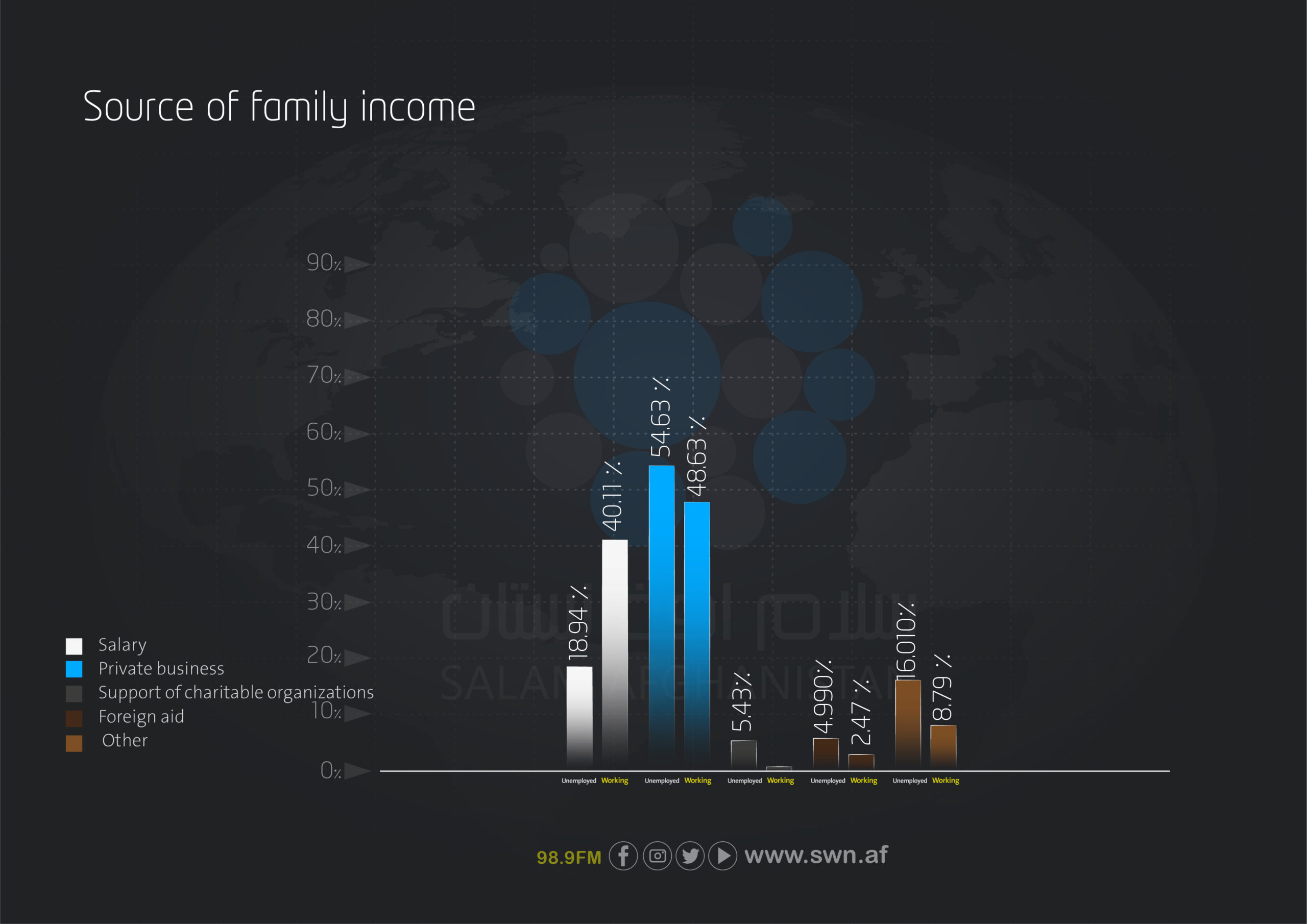

More than half of the families (52.5%) earn their income through personal businesses, while about one-fourth (26.3%) receive a fixed salary. Foreign aid and charitable contributions play a smaller role, accounting for less than 8%. This indicates that families mainly rely on personal economic activities for income.

The survey findings also show that 72.4% of respondents have no capacity to save. Only 3.6% save regularly, and 23.9% are able to save very limited amounts. These statistics reflect the severe financial pressure and lack of capacity for financial savings among most families.

The survey findings indicate that nearly 75% of participants (722 women) reported a decline in their purchasing power over the past one to more than three years. This shows that the economic crisis in recent years has consistently had a negative impact on household purchasing power. On the other hand, 24.9% of respondents stated that they have had limited purchasing power from the beginning and have never been able to fully meet their needs.

Comparative analysis of unemployed and employed women regarding income sources, economic status, and purchasing power

Source of family income

This section presents that the primary sources of family income differ between unemployed and employed women. Employed women rely more on fixed salaries, whereas unemployed women are more dependent on family-run businesses and charitable assistance.

Main provider of family income

According to the survey findings, in families of employed women, the women themselves play a more significant role in providing income. In contrast, in families of unemployed women, male family members contribute the majority of the household income.

Monthly household income

Monthly household income is generally higher among employed women, with a smaller proportion of families earning less than 5,000 Afghanis. In contrast, unemployed women are more represented in households with lower incomes.

Sufficient income for living expenses

Most employed women consider their household income to be barely sufficient, but a portion of them feel that their income is fully sufficient, which is twice the proportion of unemployed women reporting the same. Unemployed women suffer a higher degree of income insufficiency.

Consumption of family income

In both groups, the majority of income is spent on food, clothing, and children’s education. However, unemployed women allocate a larger portion to food and healthcare, while employed women place more emphasis on children’s education. (The responses are mixed, and the data in this section have been calculated approximately.)

Savings capacity

Employed women have a greater ability to save, but still, the majority either do not save regularly or have no capacity to save at all.

Ability to purchase basic needs

Unemployed women, compared to employed women, are more likely to have no ability to purchase basic necessities.

Items with inability to purchase

Respondents indicated that their greatest challenges in purchasing are related to household items, healthcare, and food, with many women experiencing inability in multiple areas simultaneously.

Main reasons for inability to purchase

Unemployed women reported that their own unemployment is the most important reason for their inability to buy necessities. In contrast, among employed women, reduced household income and unemployment of family members are more significant, while rising prices have a greater impact on employed women.

Timing of decline in purchasing power

Most individuals in both groups reported that their purchasing power has declined in recent years.

Final conclusion

The survey findings indicate that Afghan women’s purchasing power is heavily influenced by economic and social factors. More than 90% of participants are unable to fully meet their basic needs, and economic pressures stemming from unemployment, reduced household income, and rising prices have directly affected their quality of life. These widespread financial limitations mean that the majority of family expenditures are allocated to food, healthcare, and children’s education, leaving little room for savings or non-essential purchases.

Unemployed women face even severe challenges, with lower ability to meet basic needs and save compared to employed women. Household income relies largely on male family members and personal businesses, which increases family vulnerability during economic crises. The ongoing decline in purchasing power over recent years highlights the deteriorating living conditions and underscores the need for targeted and urgent interventions to support economically women and families.

Without creating sustainable employment opportunities, income enhancement, and economic empowerment programs for women, this livelihood crisis could lead to widening structural poverty, reduced quality of life, and increased social vulnerability. Therefore, the development of comprehensive, cross-sectoral policies with the participation of governmental, non-governmental, and civil society organizations to strengthen the economic situation of women and families should be a top priority.

Researcher and Author: Muzhdah Haidari, Journalist at Salam Watandar

Translated by: Friba Qaderi